What Is Accrual Basis Accounting?

For example, you would record revenue when a project is complete, rather than when you get paid. This method is more commonly used than the cash method. Auditors will only certify financial statements if they have been prepared using the accrual basis of accounting.

Disadvantages of cash accounting

In order to remain accurate, accrual accounting needs frequent reports generated. These are usually the monthly financial statements most business managers are familiar with, such as the income statement and balance sheet.

This shouldn’t deter you from keeping your books on an accrual basis. Most software packages make it easy to produce cash basis financial statements from accrual basis books with just a click of a button, and your accountant is well versed in how to manually adjust financial statements from accrual to cash basis if necessary. Accrual accounting recognizes adjustment of revenues that are realized by the delivery of a product or service. When cash is received the revenue needs to recorded and recognized on a balance sheet. It also recognizes expenses related to recognized revenue.

When Pike receives the $5,000, he would debit cash and credit the unearned revenue liability account. No revenues from this transaction would be reported on the income statement for this year. As the end of the year approaches, Mike is still uncertain about finalizing his order. According to the accrual method of accounting, Pike cannot record this as a sale in the current year because he didn’t earn it. No goods or services were exchanged.

Let us now look at another practical example of an accrual accounting basis. Below is the snapshot of Facebook Balance Sheet. We note that Facebook has reported prepaid expenses of $959 million and $659 million in 2016 and 2015, respectively. As per accrual accounting, the accountant records an expense or revenue when it occurs.

Similarly, an accrual basis company will record an expense as incurred, while a cash basis company would instead wait to pay its supplier before recording the expense. Accrual basis accounting applies the matching principle – matching revenue with expenses in the time period in which the revenue was earned and the expenses actually occurred. This is more complex than cash basis accounting but provides a significantly better view of what is going on in your company. If you plan to seek outside financing for your business at some point, then the accrual accounting method is most likely your best bet.

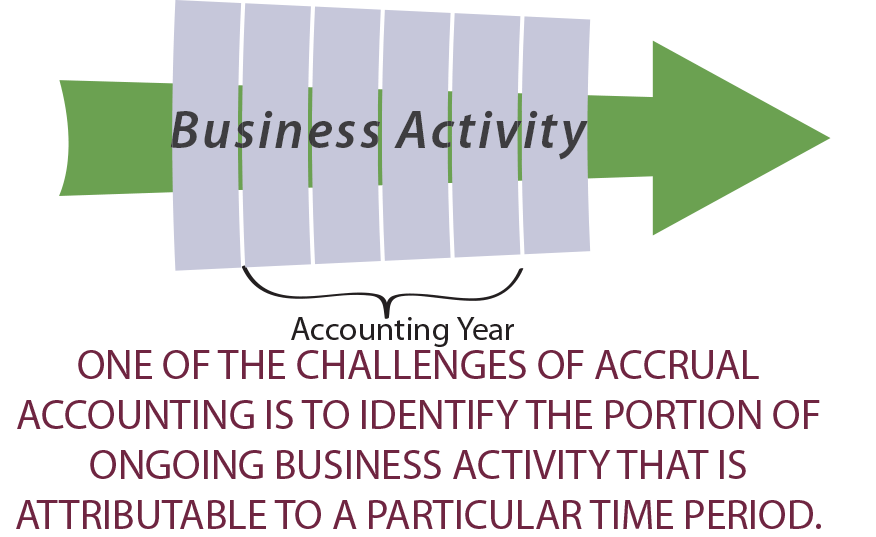

The need for this method arose out of the increasing complexity of business transactions and a desire for more accurate financial information. Selling on credit and projects that provide revenue streams over a long period of time affect the company’s financial condition at the point of the transaction.

But the credit sales will also be treated as sales and the profit would be generated by including both the cash and credit sales and then deducting the cost of goods sold and the operating expenses. Let’s say that you, an investor, want to know where a business stands at any given point in time. So what would you want to know?

- At the time of a transaction, revenues are earned by the company will credit a revenue account and will debit the asset account of Accounts Receivable.

- Auditors will only certify financial statements if they have been prepared using the accrual basis of accounting.

- For example, a company should record an expense for estimated bad debts that have not yet been incurred.

For instance, so far, the income statements in this text were for either one month or one year. Companies that publish their financial statements, such as publicly held corporations, generally What is bank reconciliation prepare monthly statements for internal management and publish financial statements quarterly and annually for external statement users. Most incorporated businesses use the accrual method.

Therefore, it makes sense that such events should also be reflected in the financial statements during the same reporting period that these transactions occur. Accrual accounting is considered to be the standard accounting practice for most companies, with the exception of very small businesses and individuals. The Internal Revenue Service (IRS) allows qualifying small businesses (less than $5 million in annual revenues) to choose their preferred method.

An investor might conclude the company is unprofitable when, in reality, the company is doing well. A disadvantage of the cash method is that it might overstate the health of a company that is cash-rich but has large sums of accounts payables that far exceed the cash on the books and the company’s current revenue stream. An investor might conclude the company is making a profit when, in reality, the company is losing money. The same principle applies to expenses.

Businesses that stock inventory, however, are almost always obligated to use the accrual method. Similarly, companies with sales of over $5 million per year must do their https://www.bookstime.com/ accounting on an accrual basis. Using cash basis accounting, income is recorded when you receive it, whereas with the accrual method, income is recorded when you earn it.

If you receive an electric bill for $1,700, under the cash method, the amount is not added to the books until you pay the bill. However, under the accrual method, the $1,700 is recorded as an expense the day you receive the bill. Expenses which can be clearly identified with the accounting period are also treated as expenses for the period even though they may not be directly associated with the revenue of that period. Such costs are regarded as period costs and are expensed in the relevant period e.g. salary, rent etc.

When is revenue recognized under accrual accounting?

Accrual method and associated adjusting entries results in a more complete and accurate reporting of a business’s assets, liabilities, equity and earnings for each accounting period. For most companies, other than very small business, accrual accounting is considered the standard accounting practice. While it does provide a more accurate picture of a business’s current condition, it is relatively complex and https://www.bookstime.com/unearned-revenue more expensive to implement than the cash accounting method. The method of accounting that measures the performance and position of a company by recognizing economic activity regardless of whether cash transaction occurs is called Accrual Accounting. Accrual accounting is an accounting method where revenue or expenses are recorded when a transaction occurs rather than when payment is received or made.

Mike simply put a down payment on an unfinished ordered. Cash accounting is the other accounting method, which recognizes transactions only when payment is exchanged. The method follows the matching principle, which says that revenues and expenses should be recognized in the same period.